How to Sell Safely Online: Payment Methods & Horror Stories

Posted by The Ban Island Team

January 26, 2023

Since I was a teenager back in 1997, I’ve been selling online. My very first exposure to selling online was on eBay (it was called AuctionWeb at that point). My mother collected Beanie Babies (she would keep them in a plexiglass case and even have a hang-tag protector!). My mother somehow stumbled upon the news that Beanie Babies were rising in both popularity and value. I vividly remember a Beanie Baby called Peanuts: a royal blue elephant. My mother found out it was worth $900 when she bought it for $10 from our local Ty store. So as a teenager, I was tasked to:

Figure out AuctionWeb

List this rare gem

Get it sold

Talk about early adoption, we were part of the first wave of online sellers.

Peanuts, the Royal Blue Elephant (Image Source and Credit: Beaniepedia)

Online marketplaces have evolved tremendously over the past 20 years. It’s a space I am deeply passionate about, and I even had two tech startups (from 2008 to 2019) solving the complex problems surrounding this. The conduction of online transactions and online payment methods have also evolved. Since March is Fraud Month, I thought I’d share a break-down on each method, including their pros and cons, and what to watch out for to protect yourself.

Some of the most common payment methods used for online transactions:

Money Orders/Cashier Cheques

Paypal

Credit Card

Bank EFTs or INTERAC E-Transfer

Wire Transfer

1. Money Orders/Cashier Cheques

USPS Money Order (Image Source and Credit: USPS)

This is the OG of online transaction payment methods. Back to those Beanie Babies in the late 90s. After our eBay transaction ended and the customer won the prized rare royal blue elephant:

They would get our mailing address

We would converse and confirm the amount

They would mail us a Money Order or Cashier Cheque

This payment method is still in circulation, and you are still able to go to any USPS (in the US) or Canada Post (in Canada) Postal office and purchase one.

👍PRO: It’s safe This is a verified way to transact as the Money orders have to be purchased with cash or debit card transactions. It can not be purchased by credit card, and thus there’s no chance of a cashback. As a seller, it’s a safe way as the funds are “guaranteed.”

👍PRO: It’s available in any currency You can also go to any international bank and buy a cashier’s cheque - also known as a traveller’s cheque. Exactly like the postal office money orders, it can only be funded through cash and direct debit transactions through the bank so there’s no risk of chargeback, and you can purchase this in any currency.

👎CON: It’s slow After receiving this money order mailed to us via snail mail, I would then deposit them into the bank. Once the money order clears (depending on your bank it may clear instantly or in a 5-10 day period), we then ship out the Beanie Babies. With snail mail, the bank clearing period, and the possibility of having to visit a bank in person to make the deposit, it can take up to 20-30 days for you to actually receive the funds in your bank account.

👎CON: There are fakes out there Like anything with value, there are always counterfeits around. Beware of fake money orders and fake cashier cheques that look and feel like the real thing. Always deposit the money order first, and wait until it clears before shipping any goods. The biggest tell-tale sign is when the scammers try to rush the shipment of the goods (coming up with many excuses), and inevitably their fake cheques do not clear at the bank level.

2. Paypal

Paypal quickly rose to popularity around 1999-2000, a few years after I had scaled up our Beanie Babies eBay operation. I first heard about Paypal when all the other auction listings would offer it as a payment option. Money orders and Cashier Cheques were no longer preferred as everyone was stating “Paypal and okay, Money order accepted”

We would also get $5 for inviting someone to try Paypal, so like the early Facebook invites, I would get bombarded with customers, or sellers alike inviting me.

[Name] invited you to join Paypal, do you want your $5, accept their invitation here.

I’ve always been an early adopter so it didn’t take long for me to accept the $5 and start inviting others. 👍PRO: It’s fast Compared to what was common at the time (the previously mentioned Money orders and Cashier Cheques), Paypal of course seemed like a dream. You get a payment from a customer within minutes - WOW! No more waiting by the mailbox, and no more visits to the bank.

👎CON: New seller account limits Every payment method mentioned on this post has its own fees, and in another post I can break down all the latest fee structures. For now, I will focus on other disadvantages including Paypal’s account limits.

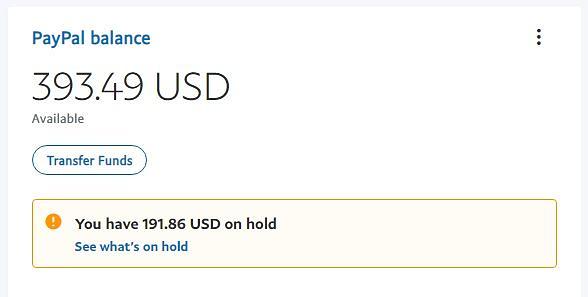

As a new seller, Paypal will place a limit on your account whereby you have to complete the first, initial transactions without getting the payment/funds prior.

Image Credit and Source: Paypal Community

For example, if Amy sent you $500 for a Chanel wallet, it will say “Pending” on the transaction. Your Paypal account will be “on hold” for the $500 in your Paypal Wallet. This means you do not have the actual payment/funds in your account, and you can not withdraw that $500.

What do you have to do?

You have to ship the item first

Add a tracking number onto the Paypal account that indicates whether the buyer has received the item, or the item has been delivered

After 7 days, or until the buyer confirms the delivery (which may be sooner), the amount (in this example $500) is released to you.

This is certainly not great for a new seller. You somehow have to muster up the courage, and take that leap of faith, to ship out your prized item on your own dime (since you haven't gotten paid yet) hoping Paypal will release the payment/funds to you.

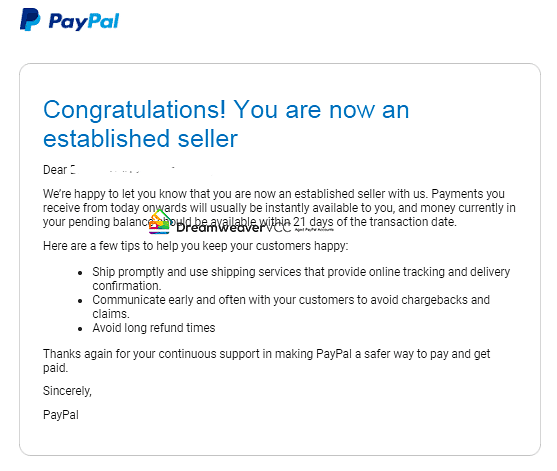

Don’t worry, this is all legit. Paypal places this a new seller limit on EVERY new seller. You will receive the payment/funds if the tracking number shows that the item has safely been delivered, and if the buyer has confirmed that they received the goods. After several of these transactions, Paypal will then give you a thumbs up and let you know that you are now an established seller removing the account limit.

Image Source and Credit: Dreamweaver

👎CON: Other Account Limits

The new seller account limit is okay especially if the first few items you are selling are of low value anyways. What’s truly annoying is the other account limits Paypal sometimes places on your account.

For a list of various reasons, Paypal has the power to put a limit on your account for almost anything.

Common reasons that trigger an account limit include:

You had a chargeback on one of your transactions

You had a claim against you or one of your transactions

Your credit card that was linked to your account was marked as stolen

We heard from your credit card that you filed an unauthorized claim

You’ve had many friends & family transactions

Your transactions have been unusually large in amount

And plenty of other reasons! All of the reasons listed above may trigger a Paypal account review which sucks because Paypal doesn’t work fast. Account reviews may take up to 21 days and your account is in a limited frozen state:

You can’t send money

You can’t withdraw money

You can’t even pay someone

I believe you can only put money in and refund someone.

Paypal conducts and resolves their own disputes and claims. Their process is slightly different than the typical credit card dispute and claim process. You can continue reading below about the credit card dispute process, but the unique Paypal factors to win the disputes are:

You must present a valid tracking number that indicates that item has been delivered to the same shipping verified address of the buyer.

Always video record the packaging of your shipment to prevent a buyer claiming they did not receive the item or that the item is grossly misrepresented.

If you do not accept refunds, say so on your listing, or on your Paypal invoice, as buyers may open refund requests.

👎CON: Exchange Rate & Default Settings I know I just said I won’t break down the fees, but I do however want to note that their exchange rate is incredibly high. AND the sneakiest thing is, their default setting is always, always, always, to exchange money. For example, I have CAD (Canadian Dollars) and USD (US Dollars) settings on my Paypal account. For me to send money to my father (he’s Canadian just like me) it will automatically take my CAD and exchange it to USD to send to him as default, unless I change the setting.

And of course, by default, Paypal selects the Goods and Services setting charging up to 2.99-5% in extra fees. You have to poke around for the Friends & Family setting where it doesn’t charge a fee. Be mindful as you maneuver the various steps and processes on Paypal, and ALWAYS use the desktop version. Their mobile version does not let you choose different exchange rates (I can only send via CAD on mobile, whereas I can choose to send USD on my desktop to avoid the exchange rate).

Paypal Friends and Family Setting (Image Source: Paypal Community)

3. Credit Card

Back in the day, it was painful to sign up for a merchant account through your bank to have the credit card processing capabilities. These days, it’s as simple as upgrading to Paypal Pro. Instead of Paypal Personal, sign up for their Business Pro account where you can create a credit card processing form on your website, or create a link that allows people to pay you via credit card. You do require to have a valid business, nor show proper documentation of it.

Image Source and Credit: JotForm

If you run a walk-in store, or even an online Shopify store, then you can simply use their built-in credit card processing option, or integrate your account with Stripe.

👍PRO: It’s universal Credit cards are one the most popular payment methods around the world with the exception of China where WePay and AliPay dominate. It’s universal; it automatically converts any exchange rate and through a click of a button, it’s processed. Within 3-5 business days, payments are deposited into your bank with sophisticated fraud detection and built-in verifications in-place which verify the billing address and the CVV.

Image Source and Credit: Technode

👎CON: Chargebacks Again, 3-4% of merchant fees aside, the biggest downside to credit card payments is its chargebacks. Depending on what you are selling, and the country your customers are from, here are the average credit card fraud rates:

Mexico: 51%

US: 46%

Canada: 32%

Data Source: Aite Group LLC

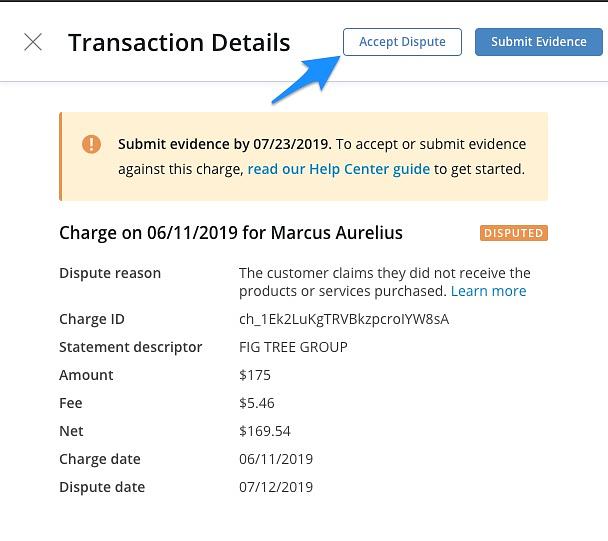

When a business receives a dispute or chargeback notification from the processing company, you have a 14-28 day window to present your argument as to why this is a valid transaction. Unauthorized Charge - Digital Goods

I’ve run several online startups where customers would pay our monthly or annual subscription using a credit card, and I’ve only won about 5% of the cases as I was not able to prove that I have delivered the goods physically. So if you are selling digital goods, always have a proof of how you have delivered your service or goods electronically.

Item Not As Described Chargebacks For any “not as described” chargebacks, these are very subjective cases to win. Ensure that you have taken photos of your product, and even produce photos or videos of your packaging, weight of your shipment, etc. These photos and videos serve as evidence, and can be presented to argue that the item is, indeed, in the condition you have stated.

Lastly, with sneakers and handbags, a lot of the disputes are based on authenticity. If your item is store-bought, make sure you have photos and copies of the original receipt that match the serial code on the bag. For any other goods, use a reputable authenticator who can prove that the item is authentic (on inauthentic) in writing for you.

Unauthorized Charge - Physical Goods

If you are shipping physical goods, like the Paypal dispute above, always ship with trackable methods with a valid tracking number that indicates that the goods have been delivered and received by the customers.

Image Source and Credit: SimplePractice Support

All Unauthorized Charges This may not be possible for all transactions, but it’s worthwhile to do so for big ticket items such as the Dior x Jordan sneakers that are currently selling for $10,000, or any luxury handbags like Hermès Birkins and Kellys that are sold on BanIsland.com.

For any large transactions, ask your customer to:

Take a photo of their IDs (Passport or Driver License)

Show their valid address (only ship there!)

Sign with a signature authorizing the charge for the tem they are purchasing (remember that the signature should match the back or their credit card)

This is the most foolproof way to win a dispute on an unauthorized charge because it’s written proof that they are, indeed, who they say they are, and they have explicitly authorized this charge.

4. Bank EFTs or INTERAC E-transfers

Image Credit and Source: echeck.org

Bank transfers can be both international or domestic, and you can do so directly through your bank, or through third party platforms like Transferwise, Venmo or Zelle. All of these are considered bank transfers when it’s from one bank to another. There is a bit of a distinction between a bank transfer and a wire transfer, and we will get into that later on.

With Bank Transfer, you are transferring using these pieces of information:

Client Name

Bank Name

Routing Number

Transit Number

Account Number

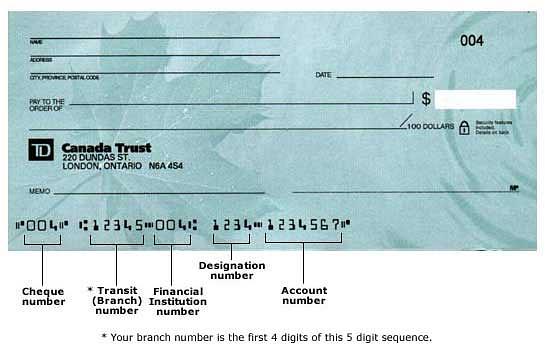

Image Source and Credit: TD Canada Trust

Sometimes you are also using a client address or bank address too, but the transaction is done through the routing number, transit number and account number (i.e., the numbers on the bottom of your cheque).

👍PRO: Fairly Simple Compared to many other payment methods, this one is fairly simple as most people have it set up and ready to go.

In Canada, almost everyone uses Interac E-transfer. You just give your email address or mobile number to one another, and for about $1.50, you can instantly send money to anyone’s bank domestically. Keep in mind there is usually a daily max of $2500 or $3000.

In the US, you can use Venmo or Zelle, and send money via email address or phone number instantly with no fees.

Venmo E-transfer Process (Image Source and Credit: Business Insider)

It doesn’t matter what bank either person uses, it’s almost instant and it transfers directly.

If you’re transferring large amounts that are above the daily maximum limit, you can go to your bank, give them the routing number, transit number and account number of the recipient, and they can do this instantly for you as well.

👎CON: EFT Reversal Happens! A lot of us think EFTs and INTERAC E-transfers are safe and irreversible. Due to Covid-19, I’ve accepted E-transfers to avoid cash handling when selling to strangers on Facebook Marketplace or Craigslist.

I thought it was secure and safe until this one incident: my EFT deposit from a buyer was deposited into my Tangerine bank account on December 14th, 2020. After that, I had shipped out my package to the buyer thinking that all was good and safe.

All of a sudden, at the end of January 2021 when I was downloading all my bank statements to give to my accountant, I noticed that there was a reversal. 😱 The full amount of $1,600 was withdrawn from me on January 29th, over 45 days later, without any notification whatsoever.

What’s worse was unlike credit cards or Paypal, there was no dispute process. I’ve had several calls with Tangerine and my bank, and the only information they were able to provide me with was “the sender’s bank sent us a request to reverse the transfer and we processed it.” They were not even able to find any information on the possible reasoning behind this reversal: why or how this happened. I asked to escalate the matter to supervisors and there’s nothing that can be done, they said.

It’s a transfer that can be reversed and if you are unlucky like me, you are just out the amount.

5. Wire Transfers

Image Source and Credit: Alibaba

I never really understood the difference between a bank transfer vs. a wire transfer until the incident above happened. I thought wire-transfer was just another way of saying bank transfer, but it is actually very different.

Wire Transfer is the ONLY form of payment that guarantees payment/funds. Meaning, yes, after 48 hours, once the payment/funds deposited into your account, it CANNOT be reversed.

It is transferred through a SWIFT/BIC code: a standard format of a Bank Identifier Code (BIC) that is used to specify a particular bank or branch. To transfer to someone, you will still need their:

Client Name

Account Number

Routing Number

SWIFT/BIC Code

It does cost more than a bank transfer. I wire transferred USD to another bank, which cost me around $45 USD, and the receipt read it cost about $17-25 USD to receive and accept. It is not a % of the amount, it is just a one-flat fee. 👍PRO: Guaranteed Funds!

This is truly the only method that is guaranteed. Once deposits are made in your bank account, there’s no way to reverse this transfer. Hopefully I am not updating this post anytime soon with new information. There is no dispute process; no one can ask their bank to reverse this.

👎CON: Fees? I struggle to come up with a disadvantage when you are able to transfer without ever losing the money, or getting a chargeback or dispute. But, there is a fee involved and you generally do have to execute by physically going to a bank.

The buying and selling processes are moving towards a more digital approach these days. With the amount of money being larger than before with luxury purchases, I hope that sharing my story and experience was helpful.

Have you tried any other newer payment methods? Please share your experience with us on our Facebook Group.

About Us

Ban Island is a luxury Hermès, Chanel and Dior community offering:

Research and collection information on all your favorite bags.

A "Have vs. Want" global request matching system, so that serious buyers and sellers can connect with one another, without any fees.

An instant visualizer tool that helps you see all the latest colors, and bring your dream bag to life.

We believe in a world where shopping and researching is FUN!